- The Mining Pod

- Posts

- CleanSpark's Mining Pool Ambitions 🌊

CleanSpark's Mining Pool Ambitions 🌊

Will it help with mining centralization?

Colin Harper

August 14, 2024 • Reading Time: 7 minutes

In a time when most miners are chasing the new, exciting thing (AI), Cleanspark has its sights set on the old, boring thing (Bitcoin mining). And that doesn’t just entail hardware and infrastructure. It also includes software.

On the Mining Pod this week, Cleanspark CEO Zach Bradford revealed that the company may bootstrap its own mining pool in the not-so-distant future, and it’s not for the reason you might think. The impetus, Bradford claimed, is not pecuniary–it’s existential.

“Will we have a pool at some point? Yes. Here’s why, and it’s not because of revenue predictability and luck, it’s because Bitcoin is going to continue to need to be diversified, and we’re going to get so big that it’s going to be important for the network – that’s why we’re going to have a pool.”

In a followup after the podcast, Bradford said that Cleanspark does “not have a set timeline, but [is] actively looking at options for how [to] roll it out.”

Cleanspark currently uses Foundry for its pool services, which Bradford called “great” and “predictable.” Foundry uses a payout method called full-pay-per-share (FPPS), so the pool operator pays miners consistently for the hashrate they deliver regardless of the pool’s luck. So even if Foundry finds 0 blocks one day, Foundry pays its miners the same amount as they would if the pool found 100 blocks that day. The payouts are based on a market rate that miners call hashprice, and the pool rewards each miner proportionally based on the hashrate they provide to the pool. If Cleanspark went it alone, Bradford said this could afford them a “negligible” bump to their revenue, but he emphasized that the monetary gain alone isn’t enough to justify the switch.

Technically speaking, if Cleanspark launches a “mining pool,” it is only a pool if it allows other miners to join it; otherwise it would just be Cleanspark solo mining. That said, we will be referring to the product (and others like it) as a mining pool for simplicity’s sake.

Cleanspark Would Join Marathon, SBI as Public Companies With Active Mining Pools

Should Cleanspark realize its own pool / self-mine, it would become the fourth publicly traded company to make this leap. Japanese financial services company, SBI Holdings, was the first to do so at the beginning of 2021 with its eponymous pool. Marathon Digital followed suit the same year with MARA Pool, and DMG Blockchain briefly ran its own pool, Terra Pool, beginning in 2022.

Marathon’s stated goal with MARA Pool was to become “fully compliant with U.S. regulations, including anti-money laundering (AML) and the Office of Foreign Asset Control’s (OFAC’s) standards,” so Marathon began excluding transactions from its blocks that were associated with OFAC-sanctioned Bitcoin addresses.

This schtick didn’t last long (less than a month, actually). Turns out, excluding transactions isn’t ideal for maximizing fee revenue. And Marathon did all this without any prompting from US officials and without any need for urgency under the laws and regulations at the time.

We reached out to Cleanspark to ask if, beyond the stated goal to encourage mining decentralization, Cleanspark also hopes to have more control over its transaction selection. Bradford said that, while transaction selection to ensure the highest fee revenue is attractive, Cleanspark does not intend to use its pool for transaction censorship of any kind.

“[That] is not our motivation. Our motivation would be to benefit the bitcoin network. We would still want bitcoin to work as it does best, which is as a peerless trusted system. From time to time, we would also benefit in high fee environments, and we would also not be subject to third-party pool fees.”

One Pool to Rule Them All

Regardless of Cleanspark’s motivations to mine its own blocks, the news enters the public forum at a time of mounting concerns over mining pool centralization.

The same FPPS payout method we described earlier has given rise to a new form of miner centralization in the form of proxy pooling. Proxy pooling occurs when a Bitcoin mining pool sells their hashrate to another mining pool, an exchange that is similar to miners selling their hashrate to pools but on a much larger scale. In doing this, the pool waives its right to construct its own block template (although, each block bears the client pool’s signature), but it earns guaranteed revenue for the hashrate in its purview.

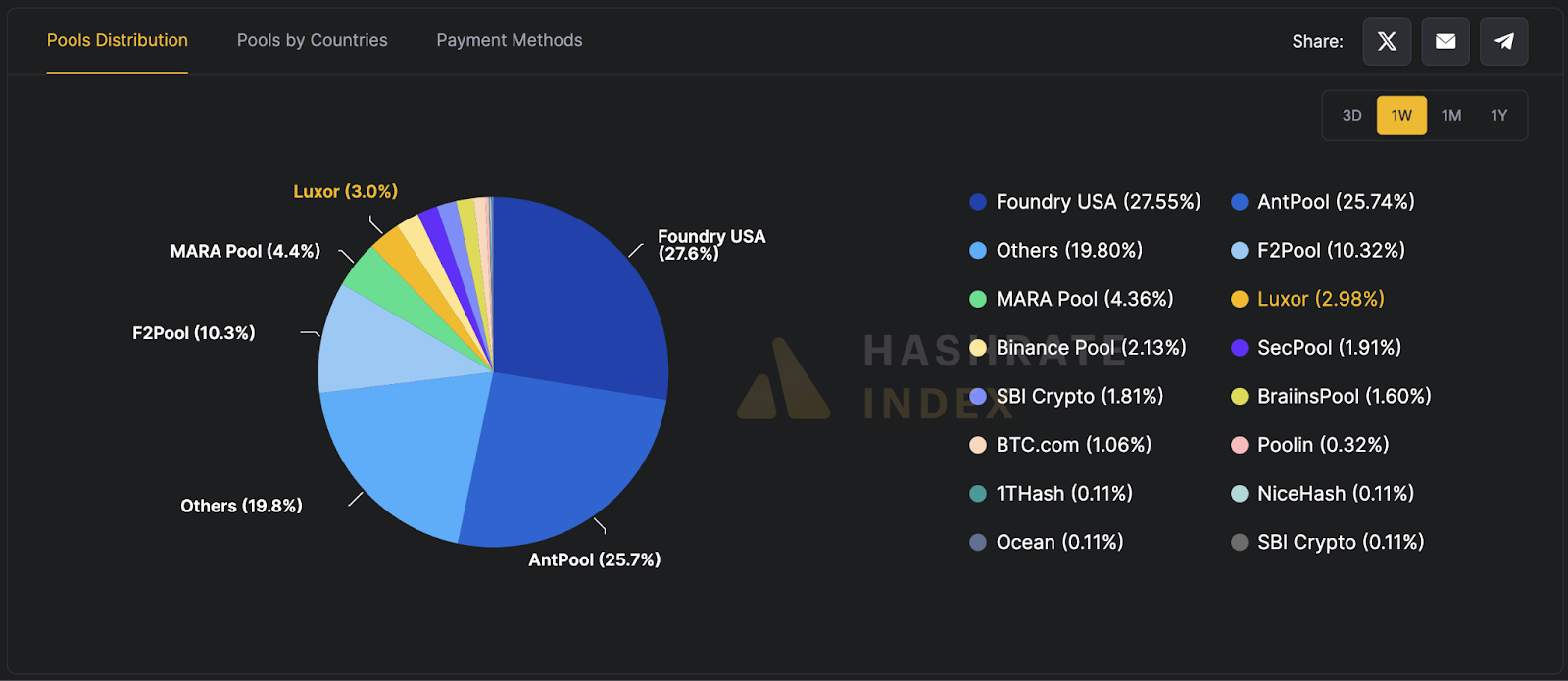

The end result? Antpool is responsible for nearly 50% of Bitcoin’s hashrate on a good day (or bad, depending on your view). Yikes.

Now, in defense of Bitcoin mining pools, it’s bad business. Specifically for FPPS pools (as well as PPS+, which is a slight variation of the same model), they are guaranteeing payouts without any solid guarantees that they will mine enough blocks to have ample liquidity. A month–a week, even–of especially bad luck could bankrupt these pools, and FPPS and PPS+ pools currently constitute 86% of Bitcoin’s total network hashrate.

Bitcoin mining pool marketshare, 1 week average | Source: Hashrate Index / Luxor

So ironically, the same rationale that attracts Bitcoin miners to mining pools is the same thing that attracts Bitcoin mining pools to other Bitcoin mining pools: steady payouts to mollify volatility.

So what can be done? Launched last year, Ocean Pool is taking a crack at the problem by giving miners the ability to construct their own templates, a feature that will soon be live on the pool. StratumV2, the next iteration of the Stratum protocol that all mining pools use to funnel all of their miners’ hashrate into a single endpoint, is another attempt from Bitcoin mining software and services company Braiins to solve the issue. But StratumV2 doesn’t give miners the full ability to construct their own block templates, only the ability to request changes or additions to the block templates that the mining pool produces. Another solution, perhaps, is industrial scale miners like Cleanspark going it alone, although in doing so, it would take away hashrate from Foundry and not Antpool.

No matter the attempted or proposed solution, proxy pooling hangs over the head of the Bitcoin mining industry and the network it maintains like a Sword of Damocles. So far, no serious ill has come of it, but it would be wise for the market to try on as many solutions as possible to avoid tragedy in the future. After all, everything is fine. Until the sword falls, that is.

But maybe the financial incentives under the current FPPS-dominated landscape are enough to woo miners into forgetting the sword is there–if not obscure it from their sight completely.