- The Mining Pod

- Posts

- The Good, The Bad, and the Ugly

The Good, The Bad, and the Ugly

The Q2-2024 financials for public bitcoin miners are in – here’s how they did.

Colin Harper

August 21, 2024 • Reading Time: 7 minutes

7 Charts To Know For Public Bitcoin Miners

Public bitcoin miners now have a full quarter behind them after the April 2024 Bitcoin Halving, and their financials are not as bad as you might expect. Now, they’re not terrible – but they’re not great, either.

The 2024 Bitcoin Halving shaved Bitcoin’s block subsidy from 6.25 to 3.125, so all else being equal, bitcoin miners took a 50% haircut on their revenue. Hashprice, a metric that measures bitcoin mining income potential, measures this best: in Q1, the average hashprice was $92/PH/Day, but this average drooped 27% to $67/PH/day in Q2. If we look at quarterly close hashprice, the situation looks even more dire: hashprice fell 57% from the end of Q1 to the end of Q2, from $110/PH/day to $48/PH/day.

Now, you wouldn’t necessarily know that bitcoin miners across the board had their income nuked in Q2 if you were looking only at stock prices (then again, you wouldn’t know that 50% of the stock market consists of unprofitable companies if you were looking at the composite indices…). Most of the big pure-play, traditional miners are down year-to-date, but a handful of “mullet miners” – those with incipient AI strategies – are actually up YTD, and not insignificantly, either.

But to ascertain which miners are in a better spot than others, we need to look beyond stock prices and dig into the numbers that these miners reported for Q2. For today’s newsletter, we’ve picked seven charts that tell the story best.

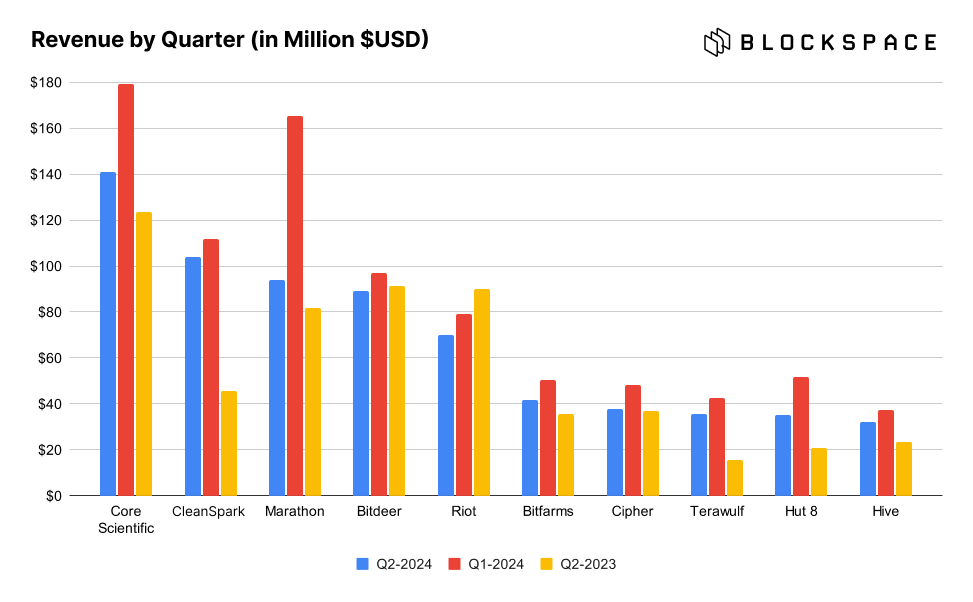

Public bitcoin miners take a hit on revenue

Let’s start with revenue.

As we covered above, hashprice is down because of the Halving (and also because transaction fee volume has dried up, but that’s another topic for another day). So naturally, we’d expect revenue to be down, as well, and that’s exactly what happened.

Source: SEC filings, presentations, press releases

Some miners were better at shoring up the Halving’s revenue reduction than others by expanding their hashrate over Q2-2024. CleanSpark, for example, grew its hashrate from 16.4 EH/s to 22 EH/s over Q2, partially from mining site acquisitions in Georgia and Wyoming. Bitdeer also grew its hashrate enough over Q2 to stanch the Halving’s impact on cash flows, as did Riot, Bitfarms, Cipher, Terawulf, and Hive.

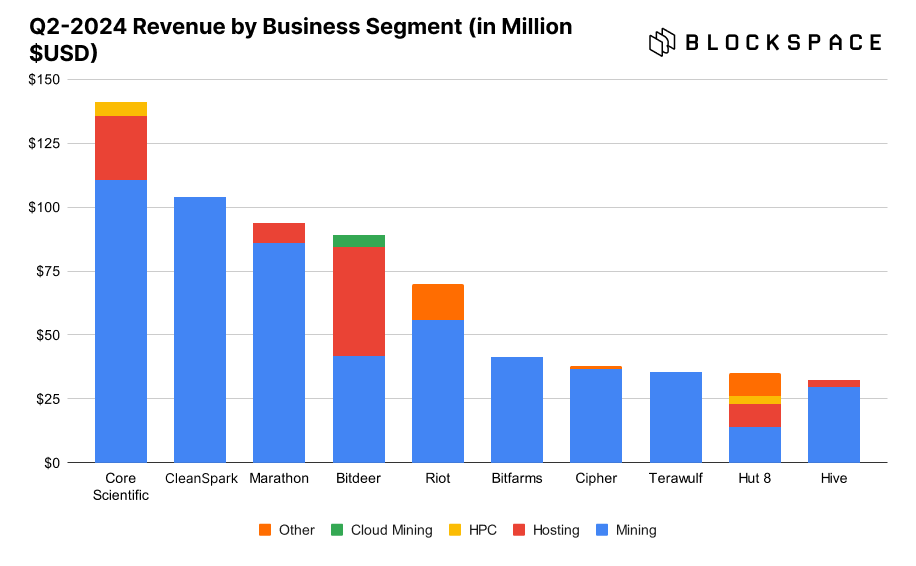

Expanding hashrate – in addition to upgrading ASIC fleets to more efficient models, which every miner is doing – is currently the most impactful strategy for offsetting the Halving. But miners have also worked to diversify their revenue streams to insulate them from this Halving’s revenue shock.

All of these alternative, non-mining related business lines are still too young to make a notable difference, and that includes artificial intelligence / high performance compute, which are have been the investment thesis darlings of the market as of late.

Source: SEC filings, presentations, press releases

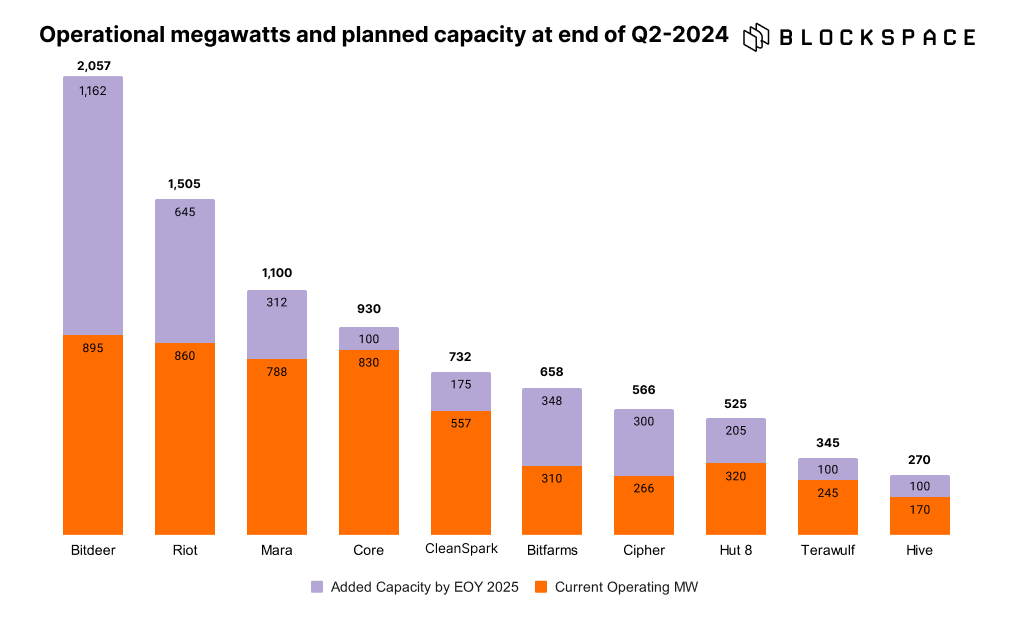

Show me the megawatts

Megawatt expansion and hashrate expansion go hand-in-hand; you can’t produce bitcoin from those factory-new ASIC miners without electricity to feed them.

The leading public bitcoin miners expanded their MW capacities aggressively last year, and they’ve continued to do so in 2024. For some, like Cleanspark and Marathon, growth came from acquiring other Bitcoin mining sites, while most others focused on expanding the capacity at their current sites or building new ones.

These public bitcoin miners have greater ambitions still for expansion through 2025, with three projecting gigawatt capacities by the end of next year. (Please note that the chart below shows current operational MWs and expect MWs based on disclosures from these miners, so they may be more-or-less accurate based on uptime and, for expansion, execution).

Source: SEC filings, presentations, press releases

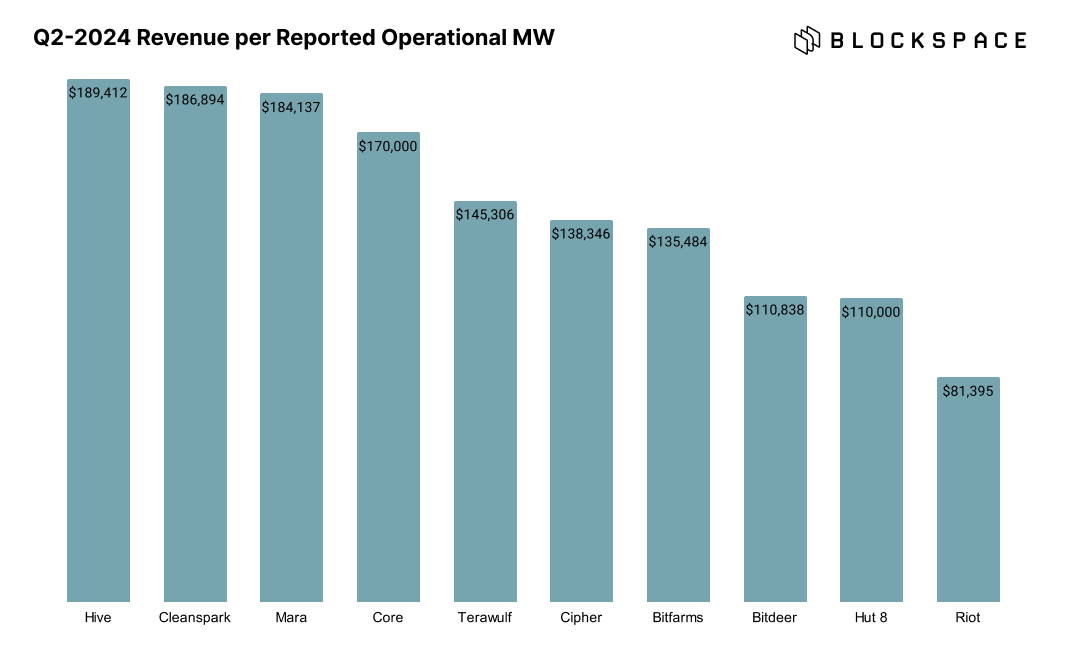

If you strip a public bitcoin miner down to its barest parts, it has one job: turn the electrons into revenue. As such, we can judge a bitcoin miner’s quarterly performance based on how much revenue it generates from its operational megawatts. With the Revenue/MW ratio, we can see which miners are more efficient at this (and thus which may be undervalued) and which miners aren’t (and thus might be overvalued).

Source: SEC filings, presentations, press releases

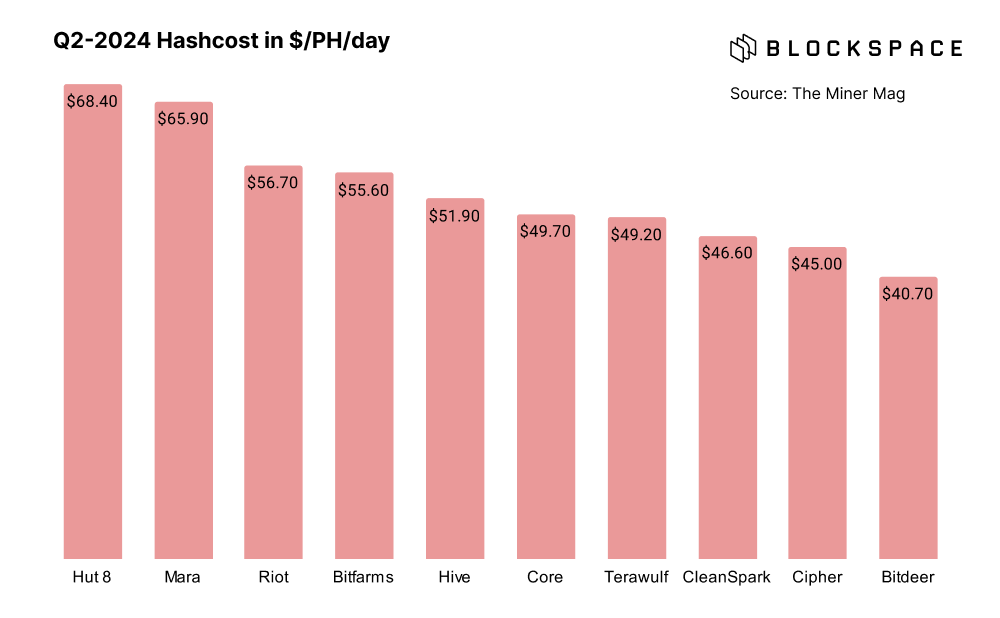

Public bitcoin miner Q2 2024 power cost, fleet efficiency, and hashcost

As we mentioned earlier, bitcoin miners can boost their revenues by adding more hashrate. But to improve profit margins and lower costs, they need to either upgrade their fleet to the most efficient ASIC miners and/or lower their power cost, the latter of which is much more difficult.

Every public miner in our update has taken pains to upgrade their fleets to the latest equipment, and all but two (Hut 8 and Bitdeer) operate fleets with an efficiency below 30 J/TH. With regard to power prices, the miners in our update all have direct power costs below $50/MWh. (Marathon and Hive are absent from the chart below since they did not report power costs for Q2-2024, but their fleet efficiencies were 25 J/TH and 24.5 J/TH, respectively).

Source: SEC filings, presentations, press releases

Hashcost, an emerging metric in public miner analysis, combines fleet efficiency, power cost, and other operational costs (like SG&A/payroll and financing costs) to provide a figure that shows the miner’s total cost to produce hashrate. Like hashprice, we denominate hashcost in $/PH/day, and we use it as a complement to hashprice to denote profitability (if a miner’s hashcost is $40/PH/day and hashprice is $50/PH/day, then the miner’s theoretical profit is $10/PH/day).

The chart below uses hashcosts provided by The Miner Mag which factor in power cost, SG&A, and financing costs from public miner disclosures. Every miner but Hut 8 had a hashcost lower than Q2’s average hashprice of $67/PH/day, but only Cleanspark’s Q2 hashcost is lower than spot hashprice ($43/PH/day) at the time of writing.

Source: SEC filings, presentations, press releases

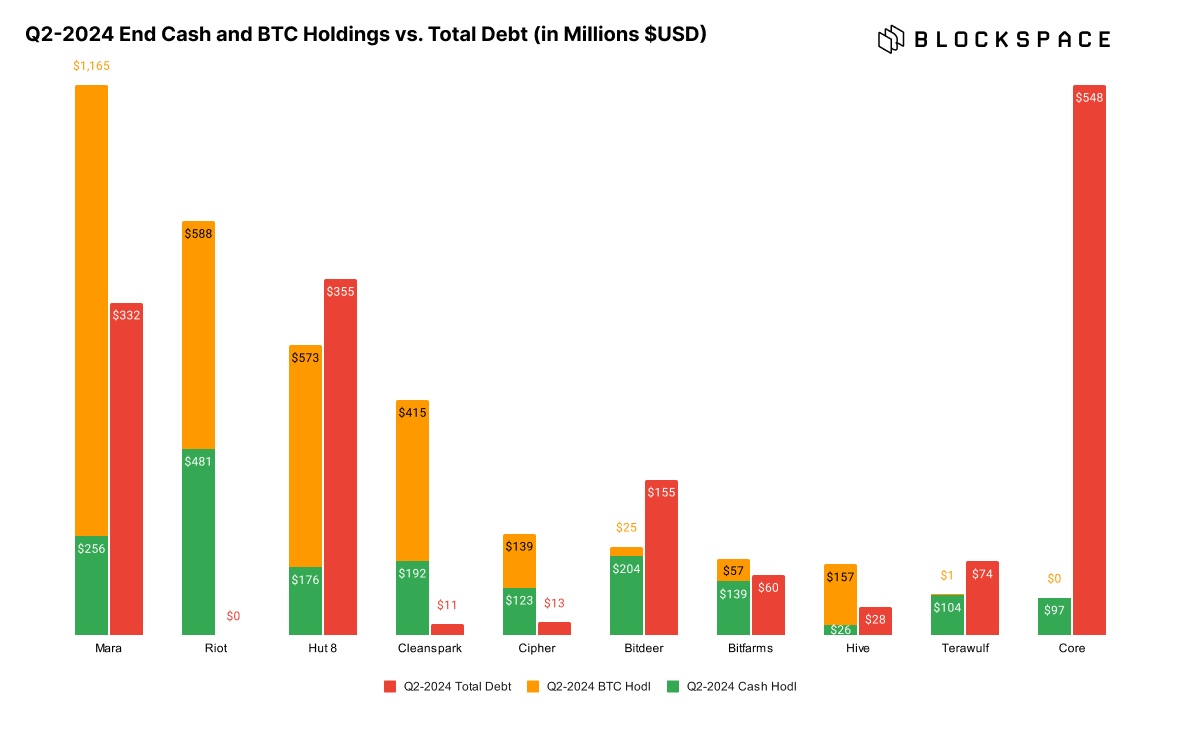

Public bitcoin miner Q2 2024 cash positions and debt

Most public miners carry modest debts, but a handful have racked up hefty bills.

Most public Bitcoin miners have enough cash and bitcoin on hand to cover their short and long term debts. Only three (Core Scientific, Hut 8, and Bitdeer) have debt that outweighs their cash and bitcoin positions.

Source: SEC filings, presentations, press releases

Thanks for reading! If you found this useful, do us a favor and reply with your favorite mining ticker!